Earned Value Management (EVM) is a project management technique for measuring project performance and progress in an objective manner.

EVM has the ability to combine measurements of scope, schedule, and cost in a single integrated system. Earned Value Management is notable for its ability to provide accurate forecasts of project performance problems.

Early EVM research shows that the areas of planning and control are significantly impacted by its use; and similarly, using the methodology improves both scope definition as well as the analysis of overall project performance.

More recent research studies have shown that the principles of EVM are positive predictors of project success.

Earned Value (EV) shall be incorporated into all projects during design phase services. In design-bid-build projects EV will be utilized from concept to the delivery of 100% construction documents.

For Design-Build projects, EV will be utilized from concept to the delivery of design-build packages.

Earned Value Analysis

Each month, the Engineer shall perform an Earned Value Analysis (EVA) using the cost and schedule software specified in Section III of this manual. The Engineer shall include the results of the EVA in the Progress Monitoring Report as described later in this section.

The EVA shall be based on the following data in the Project Design Schedule (PDS) at the data date:

1. Actual start and finish for each activity as of the data date.

2. The progress of the activities that started, but are not finished on the data date.

3. Percent complete of the work for each activity from the start date to the data date.

4. Actual cost expended for each activity as of the data date.

The Engineer’s Cost Accounting Standard Disclosure Statement shall include the procedures used to ensure the actual value of each cost account in the PDS Update was properly represented and timely recorded in the Engineer’s general cost accounting system for the design work completed by the Engineer and its sub-consultants.

If the sub-consultant actual cost data is not available prior to the submission of the PDS Update, the Engineer shall estimate the sub-consultant’s actual cost as of the data date for PDS Update. The Engineer shall confirm the actual cost from the sub-consultants prior to the submission of the next PDS Update.

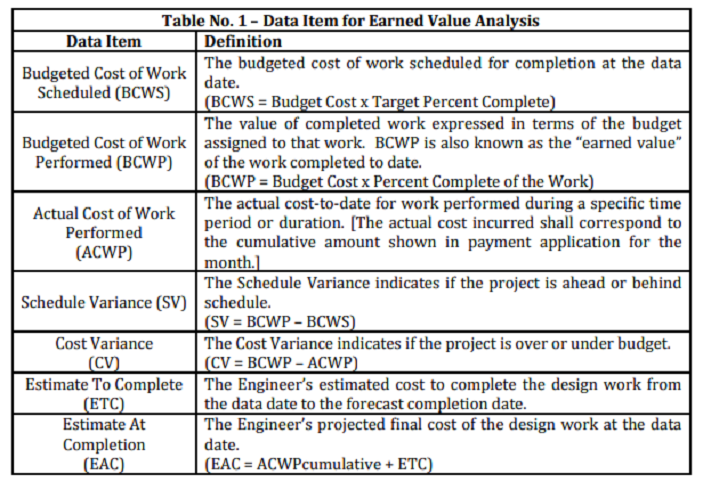

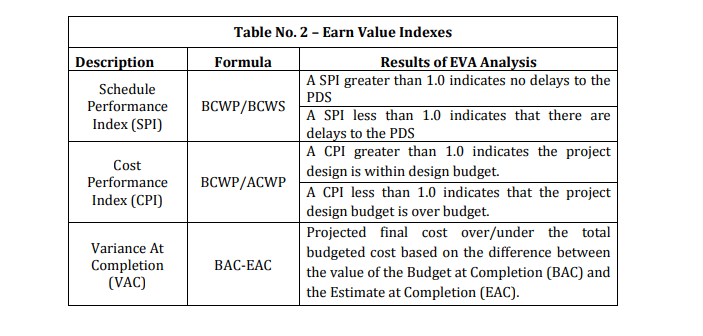

The Engineer shall use the cost accounts and scheduling data in the PDS Update to calculate and show the results of each data item in below table.

The Engineer shall determine and record the progress of work based on the results of the Schedule Performance Index and Cost Performance Index shown in below table.

The Engineer shall use Microsoft or equivalent software to provide and summarize the total values for earned valued data shown in Tables No. 1 and Table No. 2 for all activities in the PDS Update.

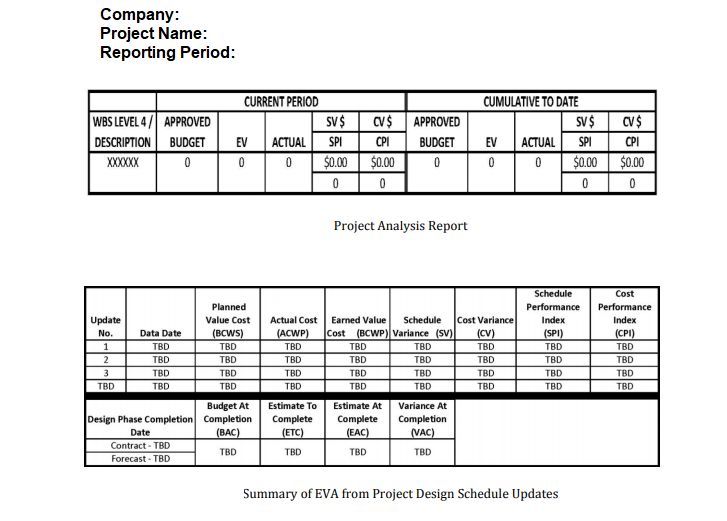

The Engineer shall provide a cost curve graphic based on the cumulative total values of the BCWS, BCWP, ACWP, BAC, EAC and VAC for each PDS Update.

The Engineer shall also show the planned BCWS from each update period to the forecast completion date. See below figure for example of a summary cost curve.

The Engineer shall prepare a project analysis report along with a summary of each update period that compares the earned value data on the data date to the cumulative total values for the EVA categories shown in below figures.

Progress Monitoring Report

The Engineer shall submit each month a Progress Monitoring Report (PMR) for the client’s review and approval.

The PMR shall contain the following information regarding the progress of work performed by the Engineer along with the earned value data.

a. Schedule Tabular Reports and Cost Control Reports, which at a minimum shall include the following:

i. Predecessor/successor report sorted by Activity ID.

ii. Early Start/Total Float sort report.

iii. Total Float/Early Start sort report.

iv. Critical Path of Work sort report.

v. Summary by Cost Account sort report

b. A description of the design work completed during the reporting period;

c. Work items and paths that are critical to the timely completion of the design phase;

d. Anticipated work to start and finish during the next reporting phase;

e. Additional design scope items;

f. Explanations of schedule delays;

g. Anticipated problems and recommended possible solutions;

h. Critical action items (listing person/agency/company responsible and date needed);

i. Explanation of the SPI and CPI results in the PDS Update submitted by the Engineer;

j. Explanation of the variances between the previous PDS Update’s SPI and CPI results to the current results (See Sample Variance Analysis Report);

k. Statement of the adequacy of the remaining design budget and time;

l. EVA cost curve graph (Similar to Figure 5); summary analysis as shown in above figure; and

m. Project analysis report for WBS Level 4 categories; and

n. EVA summary analysis as shown in above figure.

The PMR shall also include a summary that explains the Basis of Design for each phase of the design. Basis of Design shall consist of a well-defined explanation that forms the basis of the Engineer’s inspection, test acceptance criteria, expected performance, and the operational requirements designed for the project and its systems.

After reviewing the PMR and the PDS Update with the project manager, the engineer shall submit both reports with its request for partial payment application.

Revisions to Project Design Schedules that Impact Earned Value Analysis

Earned Value Analysis

The Engineer shall incorporate the cost of the proposed change(s) into the EVA, which corresponds to the proposed PDS with the fragnet. The EVA with the cost of the proposed changes shall be identified as the revised EVA for the PDSRV.

The Engineer shall perform the revised EVA in accordance with applicable contract clauses.

The Engineer shall submit a detailed report to the client for review.

The detailed report shall include the results of the EVA, the cost curve graph, and discuss the effects of the proposed change on the Engineer’s Estimate-To-Complete (ETC) and Estimate-At-Completion (EAC) along with the earned value indexes.

Upon issuance of an amendment for the change, the EVA that includes the cost for approved change(s) shall become the EVA for Revised Progress Design Schedule of Record.

Design changes shall be in accordance with the Design Change Control process. All design schedule changes shall be in accordance with Project Schedule.

Earned Value Management System Criteria

In order for an EV system to operate properly, it must, at a minimum, meet the following 10 criteria:

EVMS Criterion 1 – ANSI/EIA-748-B, 2.1(a) Organization: Define authorized work elements for the program. A work

breakdown structure (WBS), tailored for effective internal management control, is commonly used in this process.

EVMS Criterion 2 – ANSI/EIA-748-B, 2.1(b) Organization: Identify the program organizational structure, including the major subcontractors responsible for accomplishing the authorized work, and define the organizational elements in which work will be planned and controlled.

EVMS Criterion 3 – ANSI/EIA-748-B, 2.1(c) Organization: Provide for integration of the company’s planning, scheduling, budgeting, work authorization and cost accumulation processes and, as appropriate, the program WBS and organizational structure.

EVMS Criterion 4 – ANSI/EIA-748-B, 2.2(a) Planning, Scheduling and Budgeting: Schedule the authorized work in a manner that describes the sequence of work and identifies the significant task interdependencies required to meet the requirements of the program.

EVMS Criterion 5 – ANSI/EIA-748-B, 2.2(b) Planning, Scheduling and Budgeting:

Identify physical products, milestones, technical performance goals or other indicators used to measure progress.

EVMS Criterion 6 – ANSI/EIA-748-B, 2.2(c) Planning, Scheduling and Budgeting: Establish and maintain a time-phased budget baseline at the control account level against which program performance can be measured. Initial budgets established for performance measurement will be based on either internal management goals or the external customer-negotiated target cost, including estimates for authorized (but incomplete) work.

Budget for long-term efforts may be held in higher level accounts until it is appropriate for allocation at the control

account level.

EVMS Criterion 7 – ANSI/EIA-748-B 2.3(a) Accounting Considerations: Record direct costs consistently with the budgets in a formal system controlled by the general books of account.

EVMS Criterion 8 – ANSI/EIA-748-B, 2.4(a) Analysis and Management Reports: At least monthly, generate the following information at the control account and other levels as necessary for management control using actual cost data from, or reconcilable with, the accounting system:

1. Comparison of the amount of planned budget and the budget earned for work accomplished. This comparison provides the schedule variance.

2. Comparison of the amount of the budget earned and the actual (applied where appropriate) direct costs for the same work. This comparison provides the cost variance.

EVMS Criterion 9 – ANSI/EIA-748-B, 2.4(f) Analysis and Management Reports: Develop revised cost estimates at completion based on performance to date, commitment values for material and estimates of future conditions. Compare this information with the performance measurement baseline to identify variances at completion important to company management and any applicable customer reporting requirements, including statements of funding requirements.

EVMS Criterion 10 – ANSI/EIA-748-B, 2.5(a) Revisions and Data Maintenance: Incorporate authorized changes in a timely manner, recording the effects in budgets and schedules. Base changes on the amount estimated and budgeted to the program organizations.

Discover more from Project Management 123

Subscribe to get the latest posts sent to your email.